The $100bn unique insight - Letter from Hector

Every great project was once janky and obscure. They became great not by only hard work, money, or high IQ (although these help), but by uncovering unique insights.

When we see Chamath’s SPACs, or Hockney’s ‘Portrait of an Artist (Pool with Two Figures)’, we can feel that we’re missing the thing they have: their ‘flair’ or, if you’re continental, their ‘vavavoom’.

After all, geniuses’ have a vision, and they execute it.

These visions are, in fact, unique insights—each born at the intersection of simple ideas. This concept, as straightforward as it is, has implications. It means progress is layered and iterative. It impacts how we use new information and how persistent we are with the projects we work on.

Where are the secrets

Everywhere that we look and fail to look, unique insights are waiting to be unearthed. An indicator of their prevalence is in the fat-tailed distribution of outcomes.

We all know that outcomes are not directly proportional to effort. One close-to-home example is that the most popular newsletters have tens of thousands more followers than this one, even though they haven’t been going for 50,000 more years. The content, while better, is not 50,000 times more enjoyable (if it were, I wouldn’t bother).

Newsletter readership distribution is ‘fat-tailed'—the very best newsletters get all the eyeballs.

Fat-tailed distribution

Wealth distribution across the world is fat-tailed, too: the richest 0.6% hold 40% of the worlds’ wealth—the bottom 95% hold less than one third. In the health sector, Toby Ord notes of HIV & AIDS that “the best interventions [are] estimated to be 1,400 times as cost-effective as the least good.” William MacAskill, the founder of Effective Altruism, says of the charity sector that “when it comes to doing good, fat-tailed distributions seem to be everywhere.” (especially when comparing de-worming to Donkey Sanctuaries).

Likewise, a few startups create billions of dollars of value; the rest stumble and disappoint their investors.

The persistent existence of these distributions should make us hopeful. Outliers, ironically, are always there—all we have to do is work out why they occur.

Peter Thiel, in his book Zero to One, discusses the prevalence of secrets. His thesis is that secrets are everywhere: like rats in London, you’re never more than three foot from one. Blake Masters, in his essay on Thiel’s Stanford course, expands on this point:

Probably the biggest secret … [is] that there are many important secrets left. This used to be a convention forty or fifty years ago. Everyone believed that there was much more left to do. But generally speaking, we no longer believe that. It’s become a secret again.

There’s an intrinsic optimism in believing in the existence of secrets that are yet to be uncovered. For example, many systems simply don’t work: US healthcare, commercial space travel, intractable poverty in sub-Saharan Africa, and the North London Circular on weekdays. The fixes to these broken systems are secrets waiting to be discovered. I like the premise.

But, the framing of secrets as secrets doesn’t do justice to the iterative and layered approach to finding them. It suggests that the finder was lucky: you’re lucky to stumble across a secret, or you’re told about it by someone in the know. It also implies a lightbulb moment of awareness.

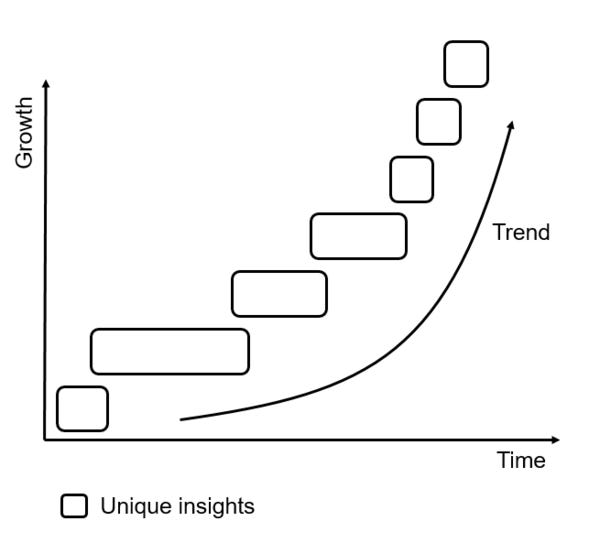

In reality, it’s more like putting a puzzle together in the dark. A puzzle made of insights, which, when combined, form unique insights. These unique insights make the fat-tailed 10,000x difference.

What we do know

There are other arguments as to why these distributions exist—and we can look at each in turn. We can be sure that it’s not time working on the problem that makes the difference; otherwise, the oldest companies would be the most successful. The opposite is true.

Similarly, it’s not capital poured on the fire of innovation that creates success. Quibi recently pulled down the shutters 6-months after launching, having raised $100 million. “Our failure was not for lack of trying,” they said, “We’ve considered and exhausted every option available to us.”

It’s not qualifications either; Oxbridge and Ivy League grads don’t lead most of the best-performing companies. Even if they did, qualifications can’t make such an extreme difference. A human brain is a human brain, after all.

So, while each of these is necessary, it’s neither capital, time, nor intellect that are responsible for the 10,000x difference between success and mediocrity. None of these could make proportionately such a vast impact. The answer is more nuanced.

Let’s now look at Coinbase through this lens. The company has escaped the gravitational pull of the startup graveyard—it’s filed its S-1 and will soon IPO. Coinbase has been valued by the private markets at $100bn, up from $8bn two years ago.

Their S-1 reads:

Customers that start with us, grow with us as they experience the benefits of the open financial system by using crypto-based products for staking, spending, saving, and borrowing. Today, our platform enables approximately 43 million retail users, 7,000 institutions, and 115,000 ecosystem partners in over 100 countries to participate in the cryptoeconomy:

Retail users: We offer the primary financial account for the cryptoeconomy – a safe, trusted, and easy-to-use platform to invest, store, spend, earn, and use crypto assets.

Crypto, while still niche, has been made accessible through Coinbase’s user-friendly frontend. Because of this, it’s attracted 43 million retail users. It’s as simple as using Transferwise (and is now valued 20x more).

Brian Armstrong, the company’s CEO, saw the opportunity to build the retail face to the crypto economy. In 2013, shortly after receiving funding from YC, Armstrong said:

“Bitcoin is a difficult technology, but we’re making it easy to use, … People keep wanting to buy more and more of it.”

This was a unique insight that few others had at the time. There were (and are) a stack of wallets out there, but they required some technical setting-up. Coinbase made it simple. With this insight, they cleared the mob and are now going public.

Today, Coinbase’s mission is:

to create an open financial system for the world. This means we want to use cryptocurrency to bring economic freedom to people all over the world.

This was not the vision when they started. It has arrived at iteratively. The mission has grown as more unique insights have been uncovered by the founding team. By way of a similarly successful example, Mark Zuckerberg understood that someone would come along and build a social network that does what Facebook does; he just didn’t expect it to be him. Even when Eric Schmidt joined Google as CEO, he was hesitant. He didn’t have faith in the insights the founders had arrived at—he didn’t think search was important and didn’t believe that the ads worked. It’s since been convinced.

These examples explain insights that are obvious to us now. But, often they are hidden—unique insights are things that founders won’t say publically. A more sinister unique insight that Zuckerberg probably had early on is that people are happy to spend hours looking at ads interspersed with their friends’ pictures.

Long-term

Unique insights are inherently uncopiable because they are arrived at through the founder’s unique journey. In that sense, because of the way they are found, they stand apart from the competition. A company is not competing with others if it is busy seeking new knowledge that intersects, building layer upon layer of unique insights.

Each layer has context the insights that came before. Each step forward leverages the existing unique knowledge that the startup has developed—the layers compound over time.

This is an iterative process, which sounds like a contradiction. How can this progressive process create 10,000x better outcomes? The unique combination (or intersection) makes an exponential difference to the original idea.

Of course, most intersections are not a good idea; for example, Geordie Shore’s and Desert Island Discs’ intersection would be awful. But, some do work, as we see in every successful business. In the context of writing online, David Perell raves about building a personal monopoly: a monopoly that exploits the unique intersection of earned knowledge. The same is true in every other domain.

What this means

As founders, our priority becomes to expose ourselves to as many new ideas as possible. These ideas will come from the zeitgeist—from customers, books, podcasts, conversations and other businesses. The ideas that intersect with the insights that we have had may make an exponential difference to our projects. Insights are found not by working harder but by increasing the chance of us arriving at these breakthroughs. Of course, this itself can be hard work.

At Yokeru, we hold a list of unique insights. I might publish this list one day, but not today.

One insight is that leaders in the care sector don’t have a place to hang out online to chat innovation. Another is that there is room for only one community-first company in each market niche. As a result, we’re building a community for innovators in care. The concept is beneficial for the users and us—we both get exposed to more ideas, which will feed more insights.

Without reading Behind the Cloud (on Salesforce), watching The Hustle’s acquisition by HubSpot, or without meeting a new friend who’s doing the same in the manufacturing space, we’d have never had this insight.